FATCA AML/KYC procedures in Hong Kong: State-of-the-art compliance?

There are two regimes in place to combat tax evasion by individuals through offshore accounts. The OECD multilateral Automatic Exchange of Information (AEoI) together with its implementing protocol the Common Reporting Standard (CRS), and the bilateral Foreign Account Tax Compliance Act (FATCA).

A third regime, the US Qualified Intermediary Regime (QI Regime) regulates the withholding of income taxes from payments of U.S. source income made to a non-U.S. person.

All these regulations have at least one thing in common – that information about certain account holders has to be identified and transmitted to the relevant tax authorities.

The question posed by this article is – can tax authorities rely on the fact that financial institutions have adequate AML/KYC and client due diligence procedures in place to populate and file the fiscal information in line with the regulations, and at the same time safeguard that they not over or underreported?

Introduction

On June 30, 2020 the OECD announced that 97 jurisdictions carried out the automatic exchange of information in 2019, enabling their competent authorities (usually a jurisdiction’s tax authority) to obtain data on 84 million financial accounts held offshore by their residents, covering total assets of EUR 10 trillion.

Because the US is not a signatory to AEoI/CRS, it is my understanding that this statistical information does not contain data exchanged under FATCA or the QI Regime and that these OECD data are therefore probably underreporting the true scale of information sharing between competent authorities.

The context of the OECD’s statistics can be seen when considering what is in scope and what is not in scope.

- CRS – Offshore accounts held by resident in a CRS reportable jurisdiction – in scope;

- FATCA – Offshore accounts held by US Citizen and US Resident – out of scope;

- QI Regime – taxation of US sourced income paid to Non-US Investors – out of scope.

Since I have spent more than a decade involved in the analysis, risk assessment and implementation of local and international measure to combat tax evasion, with this article I would highlight the following question:

Have financial institutions adequate AML/KYC and client due diligence policies in place to fulfil their reporting obligations under CRS, FATCA and the QI Regime?

Why should there are doubts?

I would like to elaborate the answer from the perspective of a Hong Kong based Financial Institution.

The 2014, FATCA temporary regulations (“2014 regulations”) required Hong Kong based financial institutions to establish AML/KYC and client due diligence procedures to identify, valid document and observe the account holder US taxpayer status and report financial accounts held by certain US persons annually to the IRS.

However, the 2014 regulations did not specify whether the term “US person” includes a dual resident.

A dual resident under the § 301.7701(b)-7 of US Internal Revenue Code (“IRC”) is an individual who is considered to be a resident in the United States (also known as lawful permanent resident) and in addition a resident in a jurisdiction under the residency article of an existing income tax treaty with the United States.

As of today, the United States have 65 income tax treaties in place.

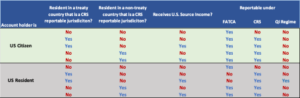

The absence of this differentiation leads to a very important point. A dual citizen with an account at a Hong Kong based financial institution may find that their personal information and account data is reported three times to the competent authorities outside of Hong Kong if their financial institution has not understood and applied the rules correctly.

They may report dual residents under FATCA on form 8966 as a US Person, on form 1042-S under the QI Regime if the dual resident generated US sourced investment income – and also since 2017 under CRS if they are tax resident in a CRS reportable jurisdiction.

US Treasury and IRS correction measures and their impacts on Financial Institutions

On January 6, 2017 the US Treasury Department and the IRS enforced T.D. 9809 “Regulations Relating to Information Reporting by Foreign Financial Institutions and Withholding on Certain Payments to Foreign Financial Institutions and Other Foreign Entities”.

Amongst other changes and enhancements, this regulation clarified that dual residents should be treated as non-US Persons to ensure consistency with the QI Regime.

This change excluded dual residents (where one of the residencies was the US) from FATCA reporting but not from FATCA AML/KYC and due diligence procedures from the reporting year 2017 onwards.

The above described changes came into effect on 06 January 2017 and are incorporated in the FATCA Rules and Regulations by enhancing §1.1471-1(b) (141).

Financial institutions should have adapted their existing AML/KYC, client due diligence and reporting procedures to identify new and pre-existing US individual account holder that fulfil the legal requirement to be treated as dual resident and to exclude them from the year 2018 onwards from FATCA reporting.

With the correct implementation of the AML/KYC and due diligence procedure the reporting results are shown in Table 3.

Findings

As tax counsel involved in the review of FATCA and CRS AML/KYC and due diligence processes for the year reporting year 2019, I can confidently say that not all tier 2 and tier 3 Financial Institutions have adapted their FATCA AML/KYC and due diligence processes as required by T.D. 9809 to identify dual residents and to ensure a tax compliant handling.

Way forward

We are all aware of the constant threat through Covid-19 here in Hong Kong, so it will not be surprising that financial institutions might not have the adequate resources available to monitor and assess the frequent changes, such as the one described for dual residents, issued by the local tax authorities, the IRS or the OECD related to tax avoidance and tax transparency regimes.

However, to be aligned with these compliance requirements, I strongly recommend tier 2 and 3 financial institutions should revisit their current AML/KYC and client due diligence processes to ensure a tax compliant reporting for the reporting year 2020.

This may be done in relation with the enhancements of the CRS due diligence procedures on beneficial owners of partnerships as announced by the Hong Kong Inland Revenue Department on April 15.

Finally, I should be mention, that by not later than 31 December 2020 the switch to the updated CRS XML format has to be finalized.

If you would like to find out how we can help you to get the upcoming activities finalized by end of 2020, please feel free to contact me for an initial discussion.