QI Status – Is It Really Worth It?

It’s an age-old question for financial institutions. Should you become a QI, or stay an NQI?

This is a decision that shouldn’t be taken lightly, but what we see more often than not is firms being told by their counterparties that they must be a QI in order to do business – which isn’t an ideal situation! So before you start down the road to becoming a QI, it’s important for you to understand what being a QI means, how it will impact your firm, and just how much resource you will need to dedicate to make it happen. Following on from our post about non-pooling and de-pooling for QI reporting, we wanted to provide a bit of insight for financial institutions potentially looking at taking on QI status.

QI vs NQIs

Before you can understand whether you should stay an NQI or take the leap and become a QI, you first need to understand the difference.

- A QI or Qualified Intermediary is a non-US financial institution that’s entered into a QI agreement with the IRS. The QI agreement is 205 pages long, so a bit of a read, but the core message is that a QI is subject to both the US tax regulations and the terms of that 205-page contract I mentioned. They can also use their QI status to grant a reduced rate of US withholding tax if their clients have claimed one. They can do all of this without revealing their client’s identity to anyone, including their counterparties and the IRS.

- An NQI is any intermediary that receives US sourced income on behalf of their clients, but hasn’t entered into the QI agreement. The overall responsibilities are the same as a QI – the difference is in the way they meet them. If NQIs want to be able to enjoy double tax treaty benefits, they have to disclose their client information to a QI. Clients of an NQI also need to be reported individually to the IRS, rather than pooling them.

Why Consider Becoming a QI?

Reputation: In 2009, the US government made it clear that any non-US financial firm that provides access to the US securities market who did not have QI status would be deemed ‘to be facilitating tax evasion’. If your institution receives US sourced income on behalf of someone else, then you’re an intermediary (by the US definition). Which means it’s a no-brainer for you to consider QI status. In fact, most firms don’t do business with NQIs, or place significant restrictions on them if they do. So, it’s usually in your best interest to opt for QI status, particularly if your clients live in a jurisdiction that has a double tax treaty with the USA.

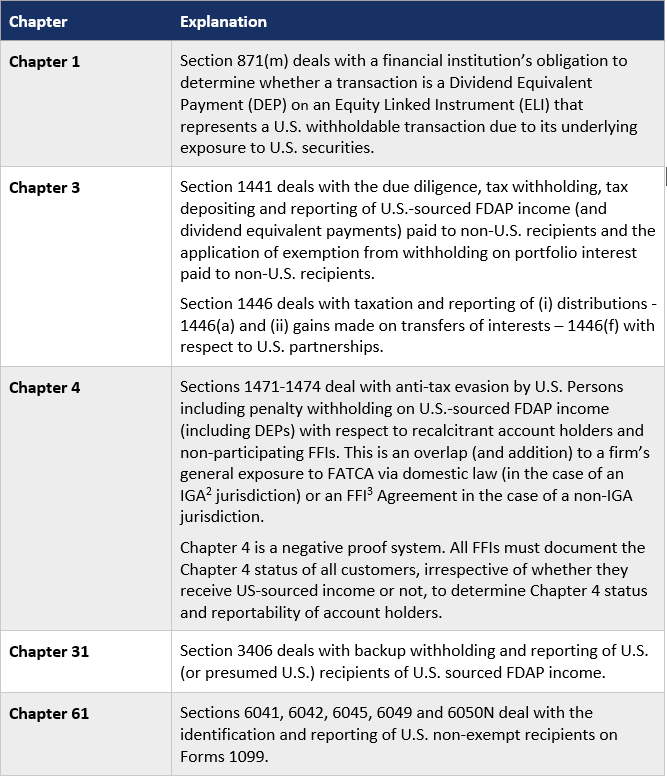

Data Privacy: The moment your financial institution starts receiving US sourced income, you automatically become subject to the US Internal Revenue Code (IRC) – in particular you may be subject to the following chapters of that code:

- Chapter 1

- Chapter 3

- Chapter 4

- Chapter 31

- Chapter 61

Exactly which chapters affect you will depend on who your customers are and what type of business you’re running. The only one that will generally impact every institution is Chapter 3, which requires any non-US intermediary to withhold tax and report payments of US sourced income they make to their non-US customers to the IRS on a form 1042-S, and file a US tax return (1042). However, NQIs aren’t trusted, and so they have to file a separate report for each and every customer, for each type of income which is much more time and labour intensive. For more information, see our blog on pooling vs de-pooling.

So, the difference here between a QI and an NQI is that a QI can protect the identity of its customers while an NQI cannot.

Tax Benefits: Only QIs can grant tax treaty benefits. The US has 68 tax treaties with other countries, which can reduce the tax burden on dividends and interest from 30% down to 25%, 15%, 10% or even 0% – great news for investors! These lower tax rates are something unique to QIs though, whose customers only need to fill in one of the US W-8 forms to get the benefits. An NQI, on the other hand, can’t grant these tax treaty benefits to their customers unless they disclose that customer to a QI – which would mean giving your customer’s information potentially to a direct competitor. Most firms aren’t too thrilled at the idea of doing this, but that means that 30% NRA (non-resident alien) tax will be withheld from the customer’s US investment income.

In other words, being a QI gives your clients a much higher level of privacy and access to lower tax rates. There is a trade-off however. While the IRS is granting QIs the authority to apply lower tax rates and not disclose who their clients are, the IRS wants to know that you’re meeting the terms of the QI Agreement. Its called control and oversight. So, in addition to the tax operational aspects of the QI Agreement, there are also compliance obligations. You will have to appoint someone in authority to be a Responsible Officer. That person will have to write a compliance program document that shows how the firm meets its QI obligations and the Responsible Officer will need to arrange the conduct of an independent review of your QI activities every three years, then certify compliance to the IRS.

In the past, we’ve come across firms (yes, plural) who believe that by remaining an NQI they’re somehow exempt from IRC Chapter 3 or worse, that because the maximum amount of tax has been withheld, that they don’t need to report. Both, unfortunately, aren’t true, and can get you into a lot of trouble. The same goes for firms that clearly act on behalf of their clients but still present a form W-8BENE to their counterparty to avoid NQI status – very illegal since the certification is done under penalty of perjury. Whichever way you look at it, if you allow your customers to trade US securities, you will be affected by the US tax regulations and have to decide between QI and NQI status. It’s a choice between protecting your clients and giving them tax treaty benefits on the one hand and having to disclose your clients or suffering the highest tax rates on the other hand.

We should note here that, even if you want to be a QI, you’re generally only eligible if you are in a jurisdiction that has had its KYC rules approved by the IRS. If you’re not, the door still isn’t closed because we can help you apply to the IRS to have those KYC rules approved, after which you can get on with your QI application.

Should You Take the Leap?

It’s no secret that since 2001 the IRS have been keen to get as many QIs signed up as possible, mainly due to the non-compliance of NQIs, who are prepared to accept their 30% tax rate and ignore their tax return and reporting obligations. You may even be one of them.

But even some quick, ‘back of the envelope’ maths shows that being a QI is the better choice. If the IRS imposed their penalties on every single NQI that failed to file their tax return, they would have charged over $100bn in fines for late report filings or worse, intentional disregard. And believe us, the IRS are indeed imposing those fines when they come across non-compliant NQIs.

If your institution has decided to take the leap into becoming a QI (or been told you have to be a QI), then the first thing you need to do is talk to a professional (us), and we can walk you through what becoming a QI really means, and how it’s done. Because while the application process might be relatively simple (and we use that word very carefully!), the consequences of becoming a QI can be very significant for your firm. Becoming a QI is about more than just paperwork – the due diligence, withholding, reporting and oversight elements – but it also impacts your firm on an operational level – rate pool accounts, withholding status vs non-withholding status and so forth – a lot of which won’t have been explained by the your counterparty – after all, you’re just their customer!

At TConsult, we spend a lot of our time helping firms understand the issues around QI and NQI status, with in-house training courses and bespoke consultation. We also provide customised support services for QIs, and support for NQIs wanting to enter the QI programme. Finally, we also offer an Exposure Map Report service which will detail your specific circumstances and how your are could be affected by US tax regulations. If you would like to know more, just get in touch with us to arrange a chat with one of our subject matter experts.