Your W-8 Questions Answered

In our last blog about W-8 forms, we talked a bit about what they are and what they’re used for. We got a lot of questions about W-8 forms off the back of that post, so today I thought it would be a good idea to gather some of them together and answer them. I promise I’ll do my best to not answer each one with ‘it depends’!

If you need an update on the basics of a W-8, click here to read the last article. Otherwise, let’s get into it.

Who Needs to Complete W-8 Forms?

Any non-US investor trying to open an account with a broker or a custodian bank will almost certainly be asked to provide a W-8 (or a W-9 if they’re American). The institution will ask you to fill one in or collect the information they need from their website (called a substitute W-8).

Which Countries Have Double Tax Treaties with The US?

This is a tricky one because double-tax treaties are changing all the time. However, I can tell you that at the time of writing, there are approximately 65 countries that have a tax treaty with the US. Get ready for a long list, because that includes:

- Armenia

- Australia

- Austria

- Azerbaijan

- Bangladesh

- Barbados

- Belarus

- Bulgaria

- Canada

- Chile

- China

- Cyprus

- Czech Republic

- Denmark

- Egypt

- Estonia

- Finland

- France

- Georgia

- Germany

- Greece

- Iceland

- India

- Indonesia

- Ireland

- Israel

- Italy

- Jamaica

- Japan

- Kazakhstan

- Korea

- Kyrgyzstan

- Latvia

- Lithuania

- Luxembourg

- Malta

- Mexico

- Moldova

- Morocco

- Netherlands

- New Zealand

- Norway

- Pakistan

- Philippines

- Poland

- Portugal

- Romania

- Russia

- Slovak Republic

- Slovenia

- South Africa

- Spain

- Sri Lanka

- Sweden

- Switzerland

- Tajikistan

- Thailand

- Trinidad

- Tunisia

- Turkey

- Turkmenistan

- Ukraine

- Venezuela

- United Kingdom

- Uzbekistan

When And Where to Submit Your W-8

No one submits their W-8 or W-8BENEs directly to the IRS. Instead, you send them back to the institution that requested it. They will then be used by the institution to decide whether to let you open an account, how to treat and tax US investment income paid to your account and whether your account is reportable under US anti-tax evasion regulations.

What’s The Difference Between W-8 And W-9 Forms?

Just to add in another issue, there’s also a W-9 form. Thankfully, it’s easy to differentiate the two.

W-8 forms are for non-residents of the US only. That includes international students, who will need to file a W-8BEN where necessary.

W-9 forms are for citizens and residents of the US. So if you’re a US resident for tax purposes, then you’ll need to provide a W-9.

How Long is a W-8BEN Valid For?

It does depend (sorry).

Provided none of the details on the form change, your W-8BEN will be valid for three calendar years from the end of the year in which you sign it. So, if you completed the form on the 28th of March 2024, it will be valid until the 31st of December 2027.

There is another quirk of the system, but it shouldn’t affect you. Your financial institution is collecting these W-8s to document your tax status under two different “chapters” of the US Internal Revenue Code – Chapter 3 and Chapter 4. The quirk is that if your financial institution is only collecting the W-8 solely to document your Chapter 4 status, then the form is valid indefinitely or until you have a change in circumstances. The three-year validity rule only applies if you’re expecting to receive US investment income into your account, so the financial institution needs to know your Chapter 3 status too.

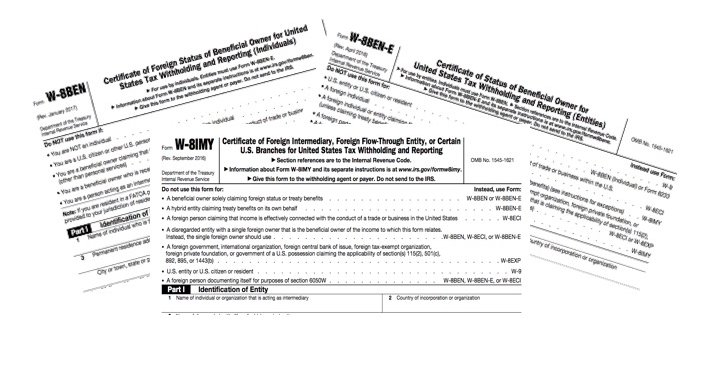

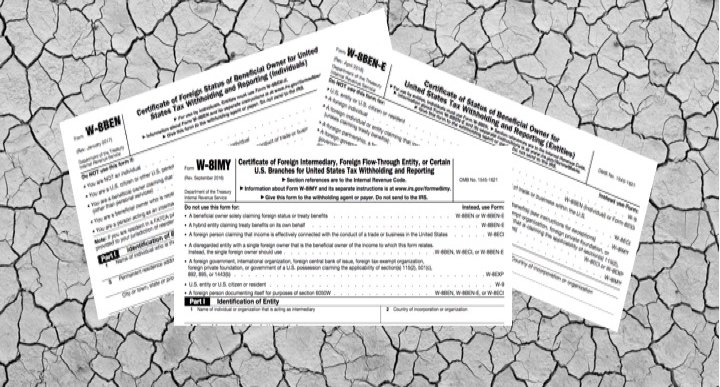

What’s The Difference Between a W-8BEN and a W-8BENE?

There are a few differences between the W-8BEN and the W-8BENE. The main one is that the W-8BENE is the form for ‘entities’, meaning any type of business or other type of institution that has more than one owner. That could be a corporation, certain types of partnership or trust, exempt entity, public and private foundations, international organisations and even foreign governments.

The default US tax rate for income received by foreign businesses is 30%, but this form will allow the business to receive a tax treaty reduction if it’s applicable and if it’s properly claimed on the form. In particular, the entity has to make a certification on the form to show that it meets what is called the limitation on benefits test.

The W-8BEN on the other hand, applies to income paid to individuals. So while the outcome is similar, the forms are aimed at different categories of people and types of account holders.

We went over these differences in more detail here.

What Happens If I Fill in the Form Incorrectly?

There are estimated to be around 900 million W-8s in circulation and about 30% are completed incorrectly in Europe. That failure rate rises to about 70% in Asia. That’s because it’s an American tax form, it’s not simple and it’s not written in plain English. Differences in language, culture and levels of understanding can affect whether you understand what you’re signing.

The big thing to recognise is that the form is signed under penalty of perjury. This means that if you fill the form in incorrectly, whether that’s deliberate or accidental, and your financial institution taxes your US income at the wrong rate, you’re the one on the hook for liability, not them.

In the end, most financial institutions are very conservative. If there is any doubt, they will tax at the maximum rate of 30%. That means that you may be over-taxed through no fault of your own. In such cases, if your financial institution is a qualified intermediary (QI), then you can ask them for a refund because their contractual agreement with the IRS obligates them to do so. If they are not a QI, then you can, in theory, file a claim directly to the IRS for a refund. The process is not simple or quick and you’ll need to ask your financial institution for a form 1042-S to prove that they over-taxed you. Then, if you’re an individual, you can file a claim on a form 1040-NR together with your 1042-S (and other supporting evidence). If you’re filing a reclaim request for an entity that was over-taxed, the form will be an 1120-F.

Who Can Help Me?

Us! At TConsult we have over 20 years’ experience in the financial services industry, particularly dealing with US withholding tax and all that comes with it. Our subject matter experts have detailed knowledge of the governments and financial institutions in over twenty-seven countries, making us perfectly placed to handle your W-8 questions and support you through the process.

We created an online platform for W-8 forms to be used by financial institutions. So, if you work for a financial institution that provides access to the US securities markets, you should get a demonstration of our Investor Self-Declaration (ISD) system. This collects all the required information for a substitute of all the W-8 forms or W-9 and makes sure that you don’t make any mistakes.

If you would like to know more, or if you’re a financial institution struggling with compliance, or you have questions about a W-8, W-8BEN or W-8BENE, just get in touch with one of our experts today.

Articles

Gain deeper insight with articles that give our considered opinion and predictions of where the industry will go next.

Publication 5262 – QI Portal

February 8, 2017Continuing the burst of activity, what better way to start a new year, than with a new QI, WP & WT portal and its bed time reading material, Publication 5262, which of course goes hand in hand with the new QI Agreement,Revenue Procedure 2017-15.Read more

Remember your New Reporting Obligations Under AEoI / CRS

May 31, 2017You're just getting over the initial FATCA and QI reporting, submitted all of your 1042-S forms, and now you're looking ahead to September and the deadline for all those 1042 forms. However, you may need to report under AEoI/CRS at the same time. Are you planning ahead to avoid this headache?Read more

3 Things To Annoy You About W-8s and 3 Things You’ll Love

July 31, 2017The IRS just made three HUGE changes to W-8 series of self certification forms used by almost every financial institution across the globe to categorise their non-US customers, and there's a lot to love...Read more

Why W8? – Start re-papering over the cracks now!

September 13, 2017QIs and NQIs face a rare opportunity to dramatically increase their W-8 compliance rate by re-papering all existing clients using the IRS' new W-8 forms. Find out how such a project could benefit your firm and why it could be worth it in the long run.Read more

Will AEoI be the new Equifax?

September 19, 2017What are the data security risks associated with the AEoI framework? In this post, Ross McGill explores some of the risks and issues a stark warning to the financial services industry.Read more

FATCA Misconceptions

November 8, 2017For some within the industry, the mere mention of ‘FATCA’ is enough to spark compliance-nightmare flashbacks. The ever unpopular FATCA regulations have now been with us for seven years. But, despite its relative longevity, there are a surprising number of misconceptions surrounding FATCA....Read more

The Challenges of GATCA

November 8, 2017The global anti-tax evasion frameworks that comprise GATCA have as many commonalities as they have differences, so it makes sense to approach regulatory compliance in a holistic fashion. In this post, we explore how smaller firms are responding to the pressures of compliance...Read more